Tecogen: Chill(ers Are) Out

Not really an AI datacenter beneficiary

Tecogen Inc (TGEN) is up roughly 4.5x year-to-date. This is mainly because the company is being viewed as a major beneficiary of the boom in AI datacenter construction.

The bull case can be roughly simplified as follows: power is the bottleneck for AI datacenters within the US and TGEN natural gas-powered chillers are perfect as they shift an enormous amount (management estimates 80% of cooling load savings; with 30-40% of overall load dedicated to cooling) of cooling load away from the grid, freeing up electrical capacity for compute. More electrical capacity for compute means more revenue for AI datacenter operators, and therein lies TGEN’s value proposition. Vertiv is a leader in data-center cooling and if TGEN could achieve a single-digit share of its revenue, it would imply multiples of the company’s current revenue base.

While some think TGEN is interesting as a long (even after the run up), I believe it is highly speculative as the downside potential is much larger than many bulls believe. Specifically, TGEN’s main products for the datacenter market - the gas-powered (Hybrid-Drive) air-cooled / water-cooled (STx/DTx) chillers - are at best a niche product as a complement to electric chillers (e.g. Trane’s CenTraVac or Johnson Controls’ YORK YZ).

This is because hyperscalers have standardized around all-electric liquid cooler architectures which combine direct-to-chip liquid (DLC) cooling and coolant distribution units (CDUs), and increasingly “chiller-less” designs. Moreover, hyperscalers have seemingly resorted to on-site power generation to relieve grid power constraints, negating the need for gas-powered chillers, whose main value proposition is power relief (i.e. “peak shaving”). Lastly, TGEN chillers have never been adopted in the datacenter market and product data sheets suggest a mismatch in specifications for said market.

Cooling Architectures

To understand why I believe TGEN’s products are likely niche, it is important to understand how datacenter cooling architectures have changed.

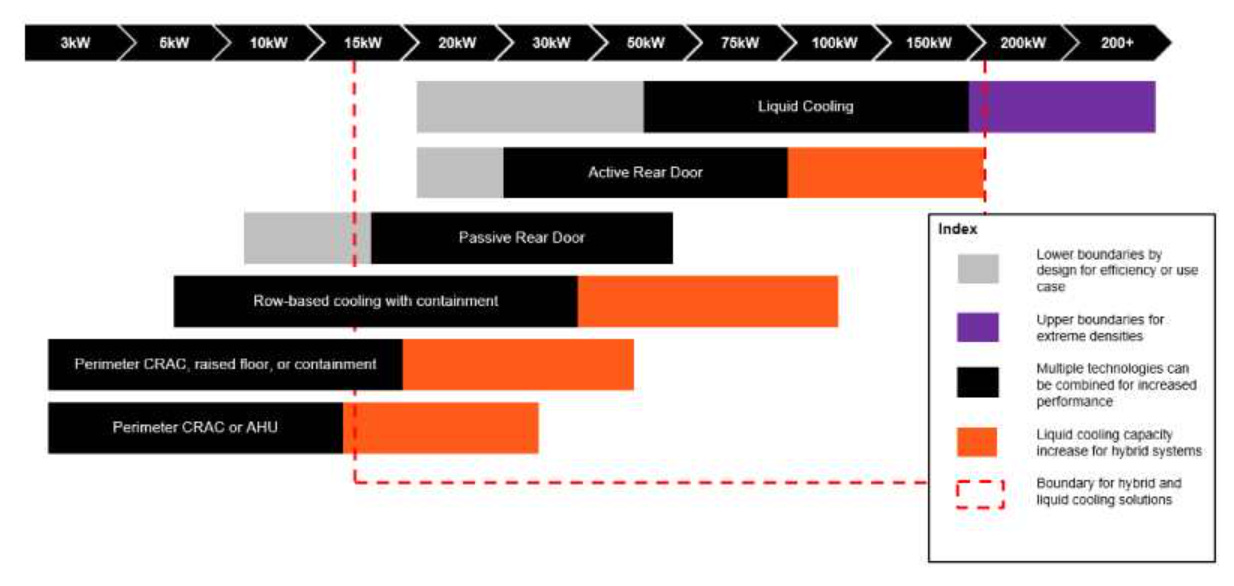

For over a decade, the standard for datacenter design revolved around racks consuming between 5 kW and 20 kW of power. These thermal loads could be effectively managed by traditional air cooling methods, such as Computer Room Air Conditioners (CRACs).1

Source: Vertiv

However, the latest generation of AI servers can draw 100 kW or even more per rack. Nvidia’s GB200 NVL72 systems, which the company has begun ramping to mass production since early 2025, specify operating temperatures between 10 °C and 35 °C, consumes roughly 130 kW per rack, and generate heat loads that exceed the limits of air’s heat transfer capacity.

At these densities, simply moving more air becomes physically and economically untenable, leading to equipment overheating, performance throttling, and potential failure. This reality has rendered air cooling obsolete for high-density AI deployments and has mandated a fundamental shift to liquid cooling as the new baseline technology.2

The predominant solution emerging to tackle extreme rack densities is direct-to-chip liquid cooling.3 In this approach, a liquid coolant is circulated through small pipes embedded in "cold plates" that are mounted directly onto the hottest components, such as GPUs and CPUs. Because liquid is thousands of times more effective at transferring heat than air, this method can efficiently capture 70% to 80% of the heat generated by the server components directly at the source.

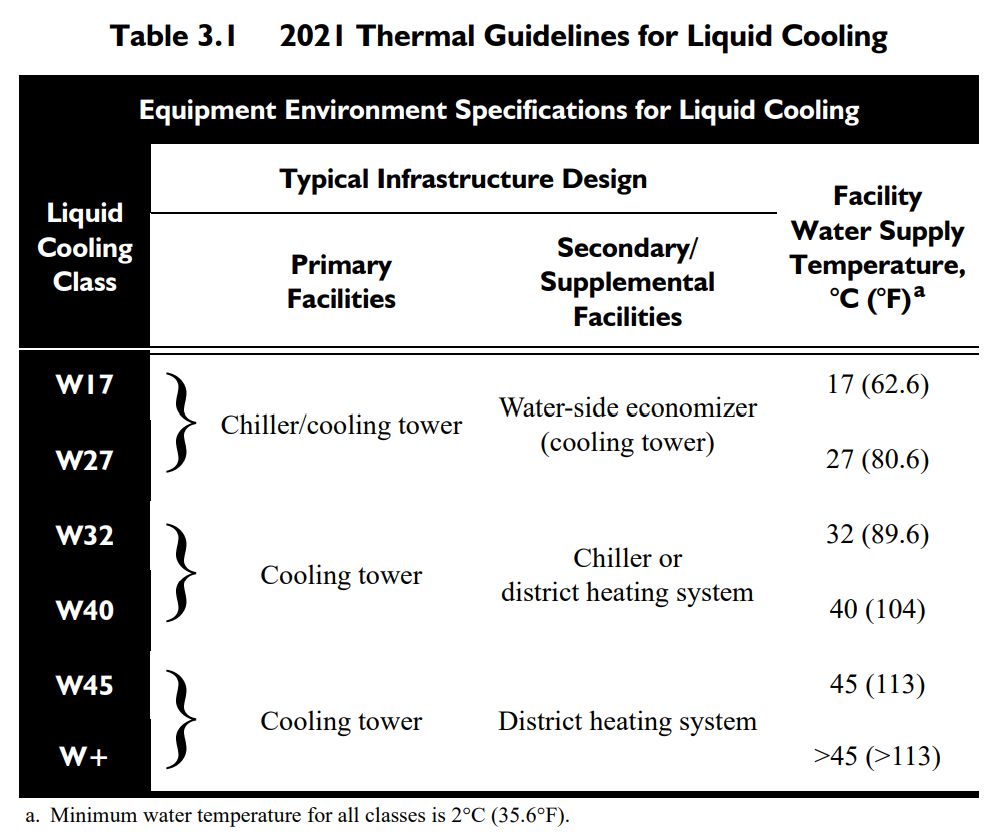

The most significant consequence of the shift to direct-to-chip liquid cooling is the ability to operate the Facility Water System (FWS) at much higher temperatures than was possible with air cooling. Traditional air-cooled datacenters required chilled water at approximately 6.7 °C to 12 °C to produce sufficiently cold air. In contrast, liquid-cooled systems can be effectively cooled with much warmer water.

Guidance from industry bodies like the ASHRAE Technical Committee and the Open Compute Project (OCP) reflects this new reality, defining new classes of liquid cooling that operate with supply water temperatures in the range of 18 °C to 32 °C, with some advanced designs pushing as high as 45 °C.4

Source: ASHRAE

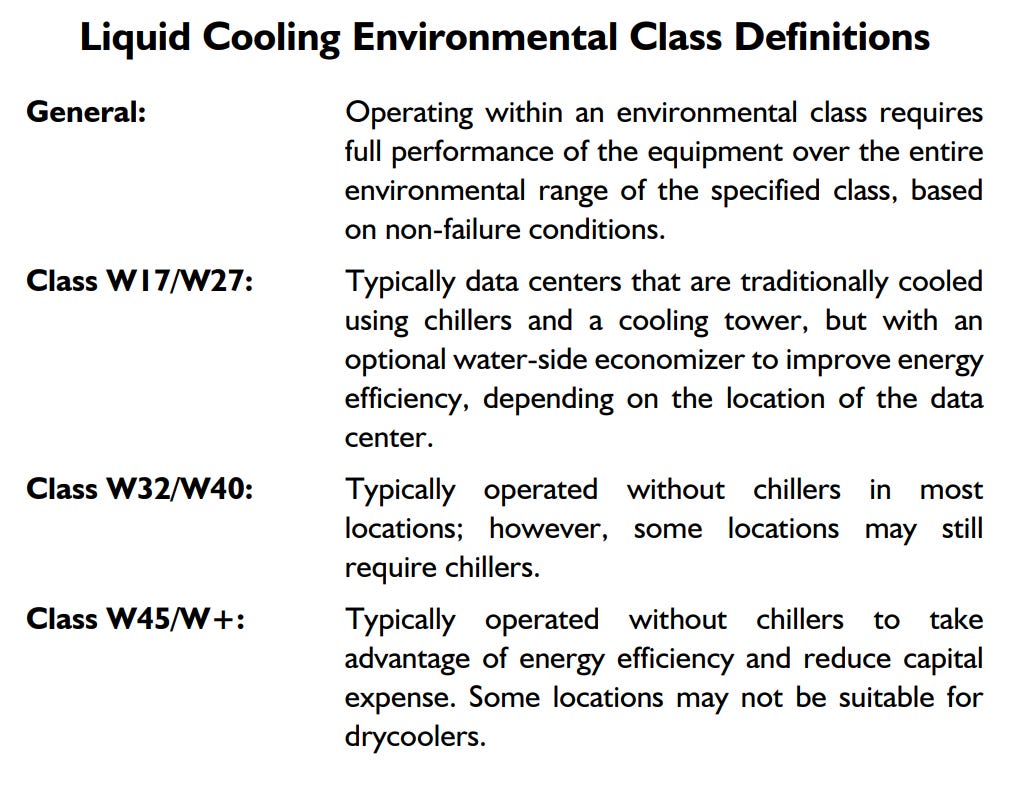

This has given rise to the "chiller-less" reference design, which is rapidly becoming the standard for new hyperscale AI builds in many climate zones. Architectures from major providers like Schneider Electric explicitly detail large-scale deployments that rely entirely on technologies like indirect air economizers, completely omitting a traditional chiller plant. Configurations include CDU/dry coolers5 and CDU/adiabatic coolers6 which offer very high energy efficiency (thus lower PUE), lower operational and maintenance complexity, and scalability. Microsoft, Meta, and Google have increasingly turned towards such “chiller-less” designs. ASHRAE environmental class definitions also suggest the most advanced datacenter designs operate without chillers.7

Source: ASHRAE. Note that these “classes” specify temperature classes in °C (e.g. Class W17/W27 covers temperatures between 17 °C and 27 °C).

On-Site Power Generation

Another reason why grid constraints do not directly represent a market opportunity for TGEN is because hyperscalers and large colocation providers are not solving their power shortages with piecemeal, load-by-load substitutions. Instead, they are solving it at the source by building or contracting for on-site power generation.

Once a datacenter campus has secured its own abundant, reliable, and often cheaper source of on-site electricity, the primary economic driver for using a gas-engine chiller evaporates. The decision calculus then reverts to selecting the most efficient, reliable, and scalable electric chiller for the cooling loop. In this context, Tecogen's solution is not competing against high-priced, constrained grid electricity; it is competing against the datacenter's own low-cost, on-site electricity, a battle it is unlikely to win on TCO.

Meta’s recent pivot in datacenter strategy relies on on-site natural gas plants to alleviate grid constraints, rather than utilizing “peak shaving” chillers. Google and Amazon are doing the same, and with tax incentives to boot.

Product Market Fit Mismatch

Across its marketing and technical literature, Tecogen consistently highlights several key performance claims. The most prominent is an "ultra-high efficiency" Integrated Part Load Value (IPLV) Coefficient of Performance (COP) of 2.6 for its water-cooled models. A second major feature is the availability of "free" waste heat recovery. The natural gas engine generates a significant amount of high-grade thermal energy (up to 230°F / 110°C hot water) from its engine jacket and exhaust, which can be captured and used for other purposes like space heating or domestic hot water.

However, these claims should be considered in the context of AI datacenter applications. The advertised IPLV COP of 2.6 is likely a standardized rating derived from AHRI Standard 550/590 (based on the specs of its other chillers), with conditions of 44°F leaving and 54°F entering chilled-fluid temperatures, which is based on conditions typical for commercial building air conditioning. Essentially, these advertised performance claims are not based on operation in an AI datacenter; operation of said chillers in different temperatures would differ from these advertised specifications. As noted earlier, architectures are shifting to accommodate higher temperatures.

It is thus unsurprising that TGEN chillers have only been sold to the non-datacenter markets. They have been sold to hospitals, government buildings, ice rinks, research laboratories, etc, but not datacenters. A full list of case studies are available here, while case studies for their water-cooled chillers are here, and air-cooled chillers are here. The order from a cloud storage data center in CT were for TGEN’s InVerde cogeneration products, not chillers.

It is also interesting to note that TGEN chillers are not certified by the AHRI. A search on the AHRI directory (Cooling and Heating (Water) -> Air-Cooled Chillers / Water-Cooled Chillers) could not find certifications for TGEN chillers compared to players like Vertiv, Trane, etc, who have many products certified. In other words, the advertised performance specifications are based on the manufacturer’s (i.e. TGEN) claims and have not been verified by independent industry-recognized third parties. Datacenter operators are required to meet stringent service level agreements (SLAs) and deploying non-certified equipment introduces significant performance risk.

Vertiv Partnership

However, TGEN recently signed a partnership with Vertiv, which is regarded as an industry leader in datacenter cooling infrastructure. TGEN has finalized their marketing plan with Vertiv and expects to roll this out in 3Q/4Q 2025.8 The expectation is that the Vertiv partnership provides a crucial go-to-market motion for TGEN, at scale, which TGEN severely lacks.

Interviews with Vertiv employees suggest that chillers are a product that they have a much smaller presence compared to their competitors, and hence they did the Tecogen deal.9 The deal is exclusive for products sold outside the US and conditionally exclusive within the US upon the achievement of certain unspecified sales targets.

Schneider Electric, another major datacenter cooling infrastructure provider, trades at 3.5x EV/TTM Sales whereas Vertiv trades at 5.4x. TGEN is at 8x. Both Schneider and Vertiv are much larger and thus more mature businesses, with Vertiv growing meaningfully faster at 20%+ vs Schneider at high single-digits. In other words, it seems reasonable to expect a “mature” multiple of 3-6x EV/Sales for TGEN.

This would imply that, normalized for maturity, the market is currently expecting TGEN to roughly double its revenue base over the next few years. In its 2Q 2025 call, TGEN noted they have signed a letter of intent for a 100 MW+ data center project involving 6 chillers, with potential to expand to 500 MW.10 Further, management also mentioned they were quoting on two projects which could result in 60-100 chillers per project and were in preliminary stages for another two >400 MW projects.

Risk/Reward

Such levels of interest suggest that a material market outside of hyperscaler new builds could potentially be addressed by TGEN chillers. However, there is significant risk in that such interest do not convert into purchase orders and revenue; interviews with Vertiv employees suggest that the company thinks TGEN chillers potentially has applications in AI datacenters, but are waiting for confirmation from the industry; the partnership with TGEN is optionality on securing exclusivity with a potentially key supplier if the market does indeed demand its chillers.11

In its 4Q 2024 call, management noted that illustratively, every 50MW would represent between $13-$16 million in revenue, implying $26-$32 million in revenue if this LOI were converted into an actual purchase order.12 On a TTM basis, TGEN generated roughly $26 million in revenue, and hence this one deal could justify the current valuation.

If the two aforementioned projects they were quoting on materialized into POs, TGEN revenue would grow by multiples (and likely its valuation would too). As noted, the company has yet to receive firm purchase orders, and given the dynamics outlined earlier, there is significant risk these do not convert, which would crater TGEN’s valuation as market expectations appear to price in significant orders. Risk/reward is hence skewed to the downside, and thus a long position in TGEN is highly speculative.

https://www.vertiv.com/en-us/about/news-and-insights/articles/educational-articles/high--density-cooling-a-guide-to-advanced-thermal-solutions-for-ai-and-ml-workloads-in-data-centers/

https://www.hpe.com/us/en/newsroom/blog-post/2024/08/liquid-cooling-a-cool-approach-for-ai.html

https://www.supermicro.com/en/glossary/direct-to-chip-liquid-cooling

https://www.ashrae.org/file%20library/technical%20resources/bookstore/supplemental%20files/therm-gdlns-5th-r-e-refcard.pdf

This configuration pairs in-row CDUs with large outdoor radiator-and-fan units (dry coolers). Whenever the ambient dry-bulb temperature is sufficiently below the facility water return temperature, the heat can be rejected with only the energy cost of running pumps and fans. This approach offers an extremely low Power Usage Effectiveness (PUE) and, critically, uses zero water for heat rejection, making it ideal for water-scarce regions and operators focused on Water Usage Effectiveness (WUE).

A variation where a fine water mist is sprayed onto intake pads to pre-cool the air entering the dry cooler. This lowers the air temperature through evaporation, allowing the system to operate effectively at higher ambient temperatures than a purely dry system. It uses a fraction of the water of a traditional cooling tower but is more effective than a dry cooler in hotter climates.

https://www.ashrae.org/file%20library/technical%20resources/bookstore/supplemental%20files/therm-gdlns-5th-r-e-refcard.pdf

Tecogen 2Q25 Earnings Presentation

Tegus

Tecogen 2Q25 Earnings Call Transcript

Tegus

Tecogen 4Q24 Earnings Call Transcript

Disclaimer: The author's reports contain factual statements and opinions. The author derives factual statements from sources which he believes are accurate, but neither they nor the author represent that the facts presented are accurate or complete. Opinions are those of the author and are subject to change without notice. His reports are for informational purposes only and do not offer securities or solicit the offer of securities of any company. The author accepts no liability whatsoever for any direct or consequential loss or damage arising from any use of his reports or their content. The author advises readers to conduct their own due diligence before investing in any companies covered by him. He does not know of each individual's investment objectives, risk appetite, and time horizon. His reports do not constitute as investment advice and are meant for general public consumption. Past performance is not indicative of future performance.

Thank you. Looks like they are responding to you :)

https://ir.tecogen.com/sec-filings-email/content/0001537435-25-000137/faqsabouttecogenchillersfo.htm