The Death of Google Search Is Greatly Exaggerated, Probably

Why Search is probably losing less market share than feared, and why replicating an ad platform is no mean feat

Google (or Alphabet) is starting to look fairly cheap, trading at high-teens NTM P/E and mid-teens NTM EV/EBIT. In fact, given the quality of the business, it seems tough to argue for further material multiple compression going forward. With ~10% top-line growth driving high-teens EBIT and net income growth and 2-3% annual reduction in fully diluted shares, the company looks like a reasonable 20% IRR.

The big overhang here is of course LLMs. If LLMs manage to commoditize Google Search to the extent Search is a dramatically smaller business a few years out, Google is not cheap by any means.

The main debate on Search is the extent to which LLMs (mostly ChatGPT for now) can usurp Google’s market dominance. Given that Search accounts for ~56% of revenue and likely 90%+ of EBIT (depending on your assumption of YouTube profitability), this is potentially an existential issue.

Bears point to the fact that Google is likely losing substantial query share to ChatGPT, implying that this loss in query share portends the eventual loss of relevance with advertisers and thus the shifting of ad budgets away from Google. Simplistically, Search monetization can be condensed to: revenue per query x number of queries. Hence, the loss of query share to ChatGPT would seemingly lead to a smaller number of queries and lower revenue per query as Search loses relevance with consumers.

Bulls generally do not quibble with the loss in query share, but tend to emphasize a more nuanced view. While it is possible that the loss of query share could result in lesser queries, this is not always the case; if the total number of queries increase by a sufficient amount, Google could bleed query share but still have a growing absolute number of queries.

This is clearly happening. Absolute query growth has accelerated, if Google’s management comments on AI overviews and other related features, and ChatGPT adoption and engagement are anything to go by. The acceleration in query growth is huge for Google because for many years it was nearly impossible to grow this metric beyond user growth. Sridhar Ramaswamy, who had a 15-year career building Google’s ad business, noted that “it turns out that persuading people to query more is next to impossible. All of us have a certain propensity to use Search, and it varies from person to person…it's very hard to persuade them to search more.”1 So rather than being almost solely reliant on growth in revenue per query, Google is getting another tailwind.

Source: Google. Specific 4Q numbers are not provided, only full-year numbers, hence the exclusion of 4Qs.

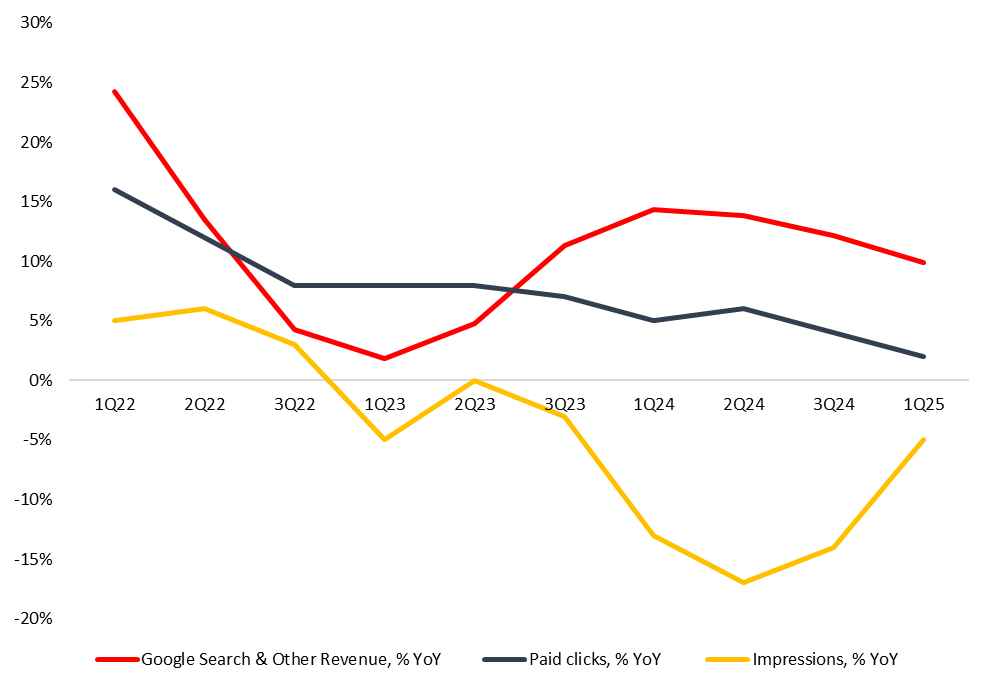

A related argument that bears are raising is the trajectory of growth in paid clicks, which has decelerated massively over the past few years. This is partly driven by extraordinarily high screen-time during COVID-19 which explains the deceleration in 2022 (paid clicks were growing 20-25% quarterly in 2021 resulting in tough 2022 comps). However, the continued deceleration has been characterized by skeptics as evidence of Google losing significant market share. In my view, the absolute market share loss is probably lesser than bears suggest. Instead, deceleration in paid clicks are driven largely by a mix shift within the business.

Source: Google. Specific 4Q numbers are not provided for KPIs, only full-year numbers, hence the exclusion of 4Qs.

While paid clicks have decelerated, impression growth has troughed in 2Q24 and is rapidly accelerating to positive territory. Part of why impression growth has been negative is likely due to share loss to LLMs, but the rate of change has clearly turned positive. The reason for the trough in 2Q24 is because AI overviews were launched in May 2024. For searches that include AI overviews, users often do not need to scroll down to the ten blue links to satisfy their query, and this naturally results in lesser paid clicks (as users aren’t clicking links) but more impressions (as users are searching more).

The key question then turns to the rate of monetization of queries with AI overviews (“AI queries”) and those without (“non-AI queries”). Google’s management has been fairly adamant that AI queries monetize at a similar rate to non-AI queries.2 This is also supported by its reported results.

Source: Google. Specific 4Q numbers are not provided for KPIs, only full-year numbers, hence the exclusion of 4Qs.

While growth in cost per click has moderated in the high-single digits, cost per impression has shown strong acceleration compared to the 2022-2023 period. Further, if AI queries were monetizing at a significantly lower rate than non-AI queries, one would expect a much more drastic deceleration in Search revenue growth.

Another argument raised by some is that the growth in cost per click and cost per impression suggests that Google could be “milking” Search. I think this argument misunderstands how Search monetization fundamentally works. Ad inventory is allocated through auctions where advertisers bid on various inventory slots, which means that the ultimate price paid is advertiser-driven.3

Building an Ad Platform Is Hard

One aspect of the current debate which is undercovered by both bulls and bears is the difficulty of building an ad platform at significant scale. This is the main risk to Search. If ChatGPT manages to build an ad platform at meaningful scale, this could potentially result in substantial advertiser budgets shifting away from Search and to ChatGPT. However, building an ad platform of such scale is costly and likely requires consumer data which ChatGPT does not have. To understand these points, it is instructive to explore how the major ad platforms scaled their businesses.

Google, Meta (Facebook/Instagram), and Amazon are the dominant players in digital advertising. Said dominance comes not just from being established in the market, but also from how they integrate large user bases, their own technology, and unique data. This data is a result of their main user activities: search and video on Google, social media on Meta, and online shopping on Amazon.

The scaling mechanisms employed by each platform, while distinct, share common foundations. They leverage powerful network effects, where growth in users attracts more advertisers, whose ad spending drives user growth, clicks, and purchases, creating a self-reinforcing loop. Each operates a highly sophisticated, proprietary ad technology stack, increasingly reliant on artificial intelligence and machine learning (AI/ML) for targeting, bidding, and measurement optimization.

Crucially, they possess deep first-party data moats, cultivated through user engagement within their "walled garden" ecosystems, providing unparalleled targeting capabilities and closed-loop attribution insights, which are particularly potent in an era of diminishing third-party data viability (courtesy of Apple’s IDFA changes and EU data privacy laws). Replicating these ecosystems presents immense challenges. Barriers to entry are exceptionally high, encompassing massive capital requirements for global infrastructure and user acquisition, the near-impossibility of matching the incumbents' scale of first-party data and network effects, and the years of iterative development invested in their complex ad tech platforms.

Google collects enormous data on user intent and interests through Search queries, YouTube viewing history, Google Maps navigation and location history, interactions within the Android ecosystem, browsing behavior via Chrome, content of Gmail messages (for security/features, not ad targeting directly), and user activity when signed into Google accounts across the web. The consequent feedback loop is very strong: more searches and platform usage generate more data, which improves search results, content recommendations, and ad targeting. Better ad relevance leads to higher advertiser ROI, attracting more advertisers and ad spending, which funds further platform improvements, attracting more users and completing the loop. Google leverages this data for sophisticated audience modeling and targeting within its ad platforms.

Meta's data moat is built on the social graph and user interactions. It collects data from user profiles (age, location, relationship status, education, work), connections (friends, followed pages/groups), content interactions (likes, shares, comments, time spent viewing), and usage patterns across Facebook, Instagram, Messenger, and WhatsApp (primarily metadata for the latter). Increased engagement and connection generates richer user profiles and understanding of social influence. This enables highly specific targeting (demographic, interest-based, lookalike audiences), driving better ad performance and ROI. Higher ROI attracts more advertisers, funding the development of new features (like Reels, Shops) that further drive engagement and data generation. Its cross-device identity graph helps track users across platforms.

Amazon possesses arguably the most commercially valuable first-party dataset, centered on direct purchase behavior. It collects data on every product search, item viewed, add-to-cart action, purchase made, wish list addition, product review written, Prime membership status, Alexa voice interaction, and video content consumed on its streaming services. More searches and purchases provide data to improve product recommendations and personalize ads. Better recommendations and relevant ads lead to higher conversion rates and sales. This attracts more sellers and advertisers to the platform, increasing product selection and potentially lowering prices, which in turn attracts more shoppers, driving more searches and purchases. The ability to directly link ad exposure to purchase activity ("closed-loop attribution") within its own ecosystem is a core advantage that becomes increasingly valuable as external tracking signals degrade.

In comparison, ChatGPT’s data on consumers likely comprise of user prompts, responses, uploaded files, metadata such as time and usage statistics, device information, operating system, browser/app used, IP address, location, account information (name, email), and payment information (if paying for a subscription). Most of this data do not really represent commercial intent, but could suggest commercial potential (e.g. knowing you use iOS and your location could help in narrowing down your potential disposable income). User prompts and responses would be where commercial intent would be shown, but anecdotally most ChatGPT queries appear to lack commercial intent and are instead more geared to knowledge acquisition or productivity enhancement. A user survey conducted by Morgan Stanley suggests limited commercial intent for ChatGPT queries:

Essentially, the data ChatGPT collects on its users is largely unproven in terms of advertising potential and driving sales. This mismatch in LLM query data and commercial intent is the largest hurdle for OpenAI, in my view. It is not enough to build an ad stack. Snap, Pinterest, and Reddit are following the major ad platforms in terms of building their ad stack, but they remain minor players in digital advertising catering to specific niches (Pinterest: visual discovery, Snapchat: AR ad formats, Reddit: community-/interest-based targeting) and are typically relegated to “swing capacity.” Even TikTok faces issues. While TikTok commands enormous user attention, translating this into monetization comparable to Google or Meta requires overcoming significant hurdles. TikTok’s data, while potent for content recommendation, lack the breadth of intent (Google) or declared interest/life-stage data (Meta) or direct purchase history (Amazon) that underpins the big three ad platforms.

Moreover, OpenAI may not have the resources to build and scale a major ad platform. Google’s TPU-driven infrastructure cost advantages has enabled it to offer much cheaper pricing than OpenAI and for more performance, potentially creating risks for OpenAI as paid users may churn to the cheaper offering. In addition, Google has enormous free cash flow from other businesses that it could use to further subsidize its LLM offerings, whereas OpenAI only has ChatGPT and is otherwise largely dependent on the kindness of the capital markets. Further, any major shift in advertiser budgets are likely to occur over a multi-year period due to the inertia and proven efficacy of the major ad platforms.

Conclusion

I think ChatGPT will continue to have a significant business in selling LLM subscriptions. Their recent effort to add ecommerce with Shopify could be a strong alternative to building an ad business, but scaling ecommerce comes with its unique set of problems (see Google Shopping, Facebook Marketplace, etc). The notion that OpenAI is an existential threat to Google appears well-supported on initial review, but there are important nuances laid out in this article that suggest the death of Google Search has been greatly exaggerated.

https://joincolossus.com/episode/ramaswamy-the-past-present-and-future-of-search/

Google 1Q25 and 4Q24 earnings call transcripts

This is a heavily simplified way in which Google’s ad auctions work as the point made does not require a more nuanced explanation. Google has historically adopted a generalized variant of a Vickrey (second-price) auction but recently switched to a first-price auction to reduce complexity, increase transparency, and render “floor price strategies” irrelevant. Both approaches achieve different outcomes, but they remain advertiser-driven.

Disclaimer: The author's reports contain factual statements and opinions. The author derives factual statements from sources which he believes are accurate, but neither they nor the author represent that the facts presented are accurate or complete. Opinions are those of the author and are subject to change without notice. His reports are for informational purposes only and do not offer securities or solicit the offer of securities of any company. The author accepts no liability whatsoever for any direct or consequential loss or damage arising from any use of his reports or their content. The author advises readers to conduct their own due diligence before investing in any companies covered by him. He does not know of each individual's investment objectives, risk appetite, and time horizon. His reports do not constitute as investment advice and are meant for general public consumption. Past performance is not indicative of future performance.